- Fitch cuts Guam’s revenue bonds to junk; S&P holds A rating

- Pacific island struggles with budget deficits, high debt

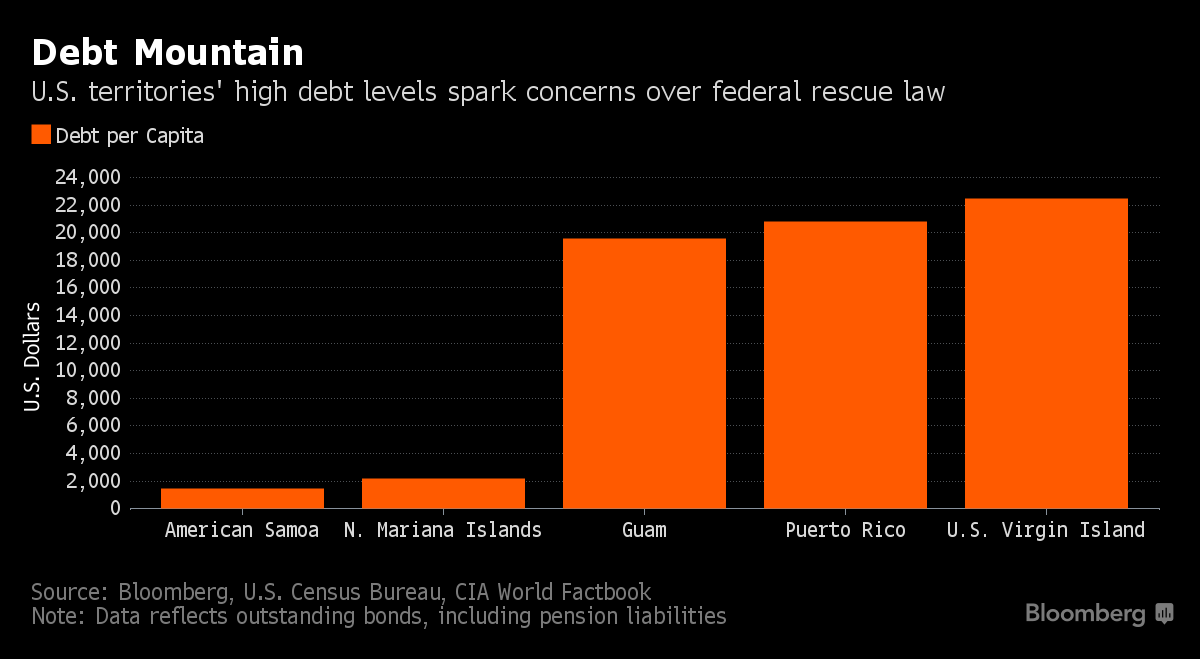

The U.S. effort to help pull Puerto Rico from a fiscal crisis has two major rating agencies at odds over another U.S. territory’s debt.

Fitch Ratings cut Guam’s business-tax revenue bonds to junk last week, arguing that Puerto Rico’s rescue law, known as Promesa, “fundamentally” alters the premise used to rate debt issued by territorial governments. Even though the act doesn’t apply to the Pacific island 9,300 miles (15,080 kilometers) from Puerto Rico, analysts say it has set a precedent that could let other territories escape from obligations to bondholders.

S&P Global Ratings disagrees. It holds an A rating on the securities, reflecting the island’s ability to pay investors.

Promesa “currently only applies to Puerto Rico. The idea that it already applies to Guam, in our view, is not correct,” said Paul Dyson, an analyst with S&P. “We have no indication that Guam is going to do something similar to Promesa.”

Unlike its Caribbean counterpart, Guam’s economic outlook is stable, according to S&P. The territory, home to American Air Force and Navy bases, stands to benefit from U.S. plans to expand its military operations on the island, which is the closest U.S. territory to potential hot spots in Asia. Representatives for Donald Trump’s transition team did not respond to requests for comment on whether the president-elect will reconsider the military buildup on the island.

Guam, however, shares some of Puerto Rico’s fiscal challenges, such as unbalanced budgets, rising pension liabilities and swelling debt. It has $3.2 billion in obligations and a population of about 165,700, according to data compiled by Bloomberg.

The possibility that other territories will be given legal recourse to cut their debts — an idea that Guam officials have repeatedly rejected — has prompted some investors to reduce their positions. Daniel Solender, head of municipals at Lord Abbett & Co., which manages $20 billion of state and local securities, said he’s sold some of the island’s debt after Promesa was enacted on June 30 and doesn’t own any of its business-tax bonds, in part because of Promesa.

“When the outcome of an investment might determined by a political process rather than the originally agreed upon terms, that makes the investment much more risky,” said Solender, whose portfolio still holds some of the Pacific island’s utility bonds. “Guam is not near that, but it opens up as a possibility now, which is hard to quantify.”

Along with the downgrade, Fitch has since withdrawn its ratings on the territory because the government decided to stop its participation in the process.

Bloomberg Markets

by Tatiana Darie

December 28, 2016, 8:59 AM PST

Written with the assistance of Bloomberg’s Municipal Global Data team.