WASHINGTON – The municipal bond market will undergo a radical transformation after the expected enactment of the tax bill, with far less volume next year, much lower demand for munis from banks and property and casualty insurance companies, and more costly and complex alternative structures for advance refundings.

This is picture painted by George Friedlander, managing partner of Court Street Group Research, in a weekly perspectives paper the group released Monday.

He said there will be more volatility in the market, a greater challenge placing bonds with lower than 5% coupon bonds with the institutional market, as well as more difficulty for small issuers selling longer serial maturities.

Friedlander said potentially there will be a greater role for exchange-traded funds and electronic trading platforms providing liquidity as well as for foreign investors and “crossover” buyers.

These are some of the impacts Friedlander and others sees from the expected passage this week of the first sweeping tax overhaul bill in three decades. The bill was released Friday evening after negotiations and agreement between House and Senate Republicans. The two chambers are expected to vote on it this week and send the bill to President Trump before Christmas.

The biggest holiday good news is that the final bill allows for the continuation of tax-exempt private activity bonds, which the House had initially proposed halting after the end of the year.

This is in line with the Senate bill, which also would have retained PABs, and it is a victory for the municipal bond market, especially since Republican conferees had discussed, but did not include, elimination of the three year carry-forward in volume cap.

The retention of PABs came after a lobbying campaign by proponents. Reps. Sam Graves, R-Mo., and Randy Hultgren, R-Ill., and 36 other colleagues urged House and Senate Republican leaders and tax-writers earlier this week to retain PABs in the tax bill because they are issued to finance infrastructure and nonprofit hospitals.

Sources say House Ways and Means Committee chair Rep. Kevin Brady, R-Texas, was a key opponent of PABs. He and other lawmakers are upset that PABs are used for projects involving corporations and other private parties, sources said. They claim there are abuses. Brady heard stories of PABs used to help finance a vineyard in California and felt that was a misuse of these bonds, the sources said.

But muni market participants claim that abuses – PABs used for massage parlors, golf courses, and McDonald’s — were shut down by the Tax Reform Act of 1986. The majority of PABs currently issued are 501(c)(3) bonds, which are used by nonprofit organizations such as hospitals and universities.

Proponents point out that PABs are a critical financing tool for multifamily and single-family housing and are used for airports, water and sewer projects, and local electric and gas facilities.

Treasury Secretary Steven Mnuchin and other administration officials in past months had proposed expanding the use of PABs so they could be used along with public-private partnerships to finance infrastructure projects. The Treasury Department had put PABs on its priority guidance plan for 2017-2018.

Muni market participants are hopeful that the administration and Congress will call for the expansion and enhancement of PABs next year as part of President Trump’s infrastructure plan, which he has promised to introduce in January.

Muni market proponents of PABs were elated at the final bill.

Tim Fisher, legislative and federal affairs coordinator for the Council of Development Finance Agencies, said, “We are thrilled that we were able to convince Congress to do something good for communities and economic development all around the country. We couldn’t have done it without our members, our partners, and everyone else who had a stake in this.”

“I’m relieved and gratified,” said Chuck Samuels, a member of Mintz Levin who is counsel to the National Association of Health & Higher Education Facilities Authorities. Usually “tax bills are like Russian novels: they’re long, boring and at the end everybody dies,” he said, “But we escaped” death.

Samuels said his group told lawmakers that if 501(c)(3) bonds were terminated, “thousands of nonprofits would either have lost access to capital or found it only at a prohibitive cost. We made it clear that some small, rural hospitals wouldn’t survive without tax-exempt financing.”

Bond Dealers of America said it “commends both House and Senate leadership for preserving the tax-exempt status of private-activity bonds in the conference report, and of governmental municipal bonds during tax reform.”

Surprisingly, the bill will also continue to allow tax-exempt bonds to be used for professional sports stadiums and arenas, which the House had wanted to eliminate as of Nov. 2 when its bill was introduced. That’s good news for stadium projects underway in Las Vegas and San Diego.

The highest-profile project is the $1.9 billion, 65,000-seat Las Vegas National Football League stadium for which Clark County, Nev. has promised $750 million of support. The venue is to host the Raiders, relocating from their longtime home in Oakland, Calif.

Also, San Diego State University is seeking to redevelop 166 acres of land surrounding the stadium formerly occupied by the NFL’s Chargers, who relocated to Los Angeles this year. While the stadium would initially be built primarily for the SDSU football team, documents released by the university add that it would “accommodate professional soccer,” and also hinted that “the stadium is also expandable should the NFL ever return to San Diego.”

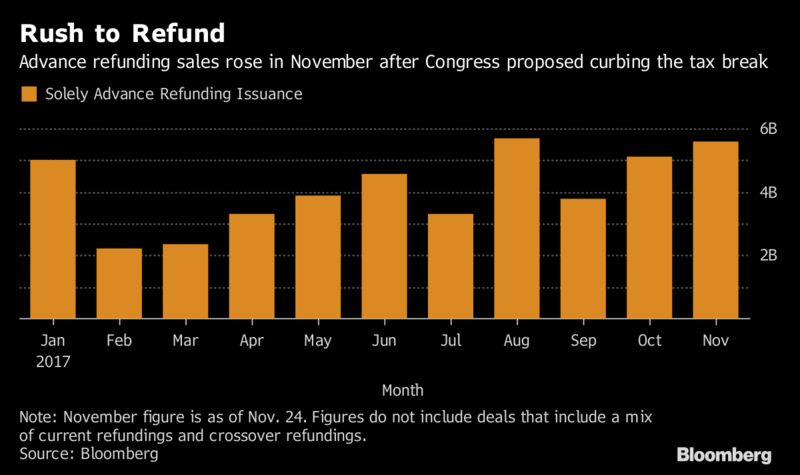

The biggest disappointment for muni issuers and other market participants is that advance refundings will be terminated at the end of the year, along with tax credit bonds.

Friedlander said the huge rush to market that has occurred with advance refundings and some private activity bond transactions will result in very slow issuance during the first quarter of 2018.

“Total supply in 2018 could easily drop 25% to the $300 billion range, as issuers who rushed to market move to the sidelines and refundings drop by close to the $100 billion range,” he said.

The halt to tax-exempt advance refundings was not a surprise because both bills had proposed that. Under current law, issuers of governmental and 501(c (3) bonds can do one advance refunding. PABs cannot be advance refunded.

Terminating advance refundings will eliminate the flexibility that muni issuers have had to take advantage of lower interest rates and free up funds for other projects. It will raise costs for issuers.

Ben Watkins, Florida’s bond finance director, said recently that his state saved $3 billion over the past 10 years by being able to advance refund its bonds.

“Obviously the advance refunding elimination is a blow,” said Samuels. “That’s significant and issuers will have to deal with that. They’ll have to restructure their financings.”

“This is a misguided attack on state and local governments that diminishes moneys for infrastructure investments, usurps local decision-making and disrespects the federal/state partnership for building America’s infrastructure, all in an effort to control the ‘cost’ of tax cuts,” Watkins said over the weekend.

BDA said, “It is disappointing … to see the repeal of municipal advance refundings retained in the conference report. The repeal of issuers’ ability to advance refund outstanding debt will result in higher borrowing costs and less flexibility when managing debt for vital capital improvement projects.”

Issuers have some alternatives to advance refundings such as shorter or more frequent calls in bond documents, taxable refundings and tax-exempt current refundings. But those alternatives also include derivative products such as forwards, options and forward-starting interest rate swaps, which would increase issuers’ their risk as well as their costs.

Muni market groups, particularly issuer groups, have been pushing lawmakers for transition rules that would delay the effective date by six months to a year, but the bill does not provide that.

National Association of Bond Lawyers president Sandy MacLennan said, “NABL is pleased that the importance of preserving private activity bonds was recognized in the final bill, however, the immediate loss of advance refundings is a disappointment.”

She added, “We will continue our collaborative efforts with other organizations to convince Congress of the value of advance refundings as an important financing tool for state and local governments, as well as non-profit organizations.”

The Government Finance Officers Association was troubled by both the advance refunding halt and the compromise on the federal deduction for state and local taxes.

“The conference report signals that Congress does not recognize certain tools, such as advanced refunding of municipal bonds, as a critical method by which issuers achieve cost savings on public infrastructure,” GFOA said. “We will continue to communicate with our federal elected officials the value these tools bring to our state and local government finance and how they ultimately serve to provide savings for taxpayers until the final vote.”

The bill offered a compromise on the federal deduction for state and local taxes. It included more a flexible, if more stringent, provision on the federal deduction of state and local taxes. It allows a deduction of up to $10,000 for state and local property taxes as well as income or sales taxes.

This was a nod to states with high income taxes like California as well as those with high sales taxes. The House bill had allowed for a deduction of up to $10,000 of property taxes. But Brady had promised California Republicans he would give them some relief from that provision. The deduction would have been eliminated altogether under the Senate bill.

“We are relieved to see that the conference committee provided $10,000 toward individuals’ ability to deduct state and local taxes,” said GFOA. “But by mapping the provision to its current use (allowing property and income or sales taxes) this signals an important byline – local tax policies are designed to satisfy the needs of local economies. The cap is a finger on the scale and is unfortunate.”

Perhaps the biggest harm to the muni market, according to Friedlander and other tax experts, will come from the 40% or 14 percentage point drop in the corporate tax rate to 21%, tax experts said.

The lower corporate rate, which is higher than the 20% rate in the House and Senate bills, will make munis unattractive to banks, property and casualty insurance companies and life insurance companies

“It’s a big deal,” said Friedlander in a recent interview. “It means the effective net benefit of owning municipals drops,” he said.

“It means a shift in the demand curve,” he added. “Munis will have to yield more relative to taxables for corporate buyers [like banks] to be willing to add them to their portfolios.”

Muni market participants will see far fewer bank loans and private placements, which have been increasingly popular in recent years, Friedlander and other sources said. That will especially hurt smaller, less frequent issuers that place bonds with banks so they don’t have to worry about credit issues and attracting the big underwriters, they said.

State and local governments are likely to see higher interest rates on their bank loans if their loan documents have corporate tax gross-up provisions that give the banks the right to increase the interest rates on the tax-exempt bonds they’ve purchased if corporate rates go down and the bonds are aren’t worth as much to them.

The individual alternative minimum tax would be retained in the tax bill but would not apply to individuals with taxable income under $500,000 and families under $1 million. The AMT applies to PABs and makes them less attractive, thereby raising their yields.

The corporate AMT would be repealed, as was included in the Senate bill. This would require corporations to pay tax on certain income not paid under the income tax such as tax-exempt bonds. All tax-exempt interest is subject to the corporate AMT, unlike the individual AMT, which just applies to PABs other than 501(c)(3) bonds.

The top individual tax rate will be set at 37%, down from the 39.6% rate in the House bill and from the 38.5% rate in the Senate bill. Brady said this would help offset the loss of state and local tax deductions for high income households.

The mortgage interest deduction would be capped at $750,000, up from $500,000 in the House bill but less than $1 million in the Senate bill.

The bill continues to treat Puerto Rico as a foreign country and is otherwise silent as far as providing relief to it. Brady said he would consider creating opportunity zones for Puerto Rico in an emergency supplemental bill. It was left out of the tax bill because it would not have complied with the Senate’s Byrd Rule, which prohibits adding to the deficit after 10 years.

Republicans have said the bill will pay for itself by increasing economic growth to 3% of gross domestic product, creating jobs, and cutting taxes for the middle class.

Democrats, however, who are incensed at having been left out of the process, including the so-called “conference committee,” complain the bill was railroaded through Congress and is a give-away to corporations. They say it will mostly benefit the wealthy, hurt the middle class, and increase the federal deficit. The bill is expected to add about $1.5 trillion to the deficit over 10 years according to the Joint Committee on Taxation.

The bill is to be voted on along party lines, with most Republicans expected to vote yes and most Democrats no. The goal of the GOP is to give the bill to President Trump to sign before Christmas.

The votes have been lined up in the Senate. Sens. Marco Rubio, R-Fla., and Mike Lee, R-Utah, who had threatened to oppose the bill unless the child tax credit was expanded, obtained additional benefits for working families on Friday and said they would support the bill.

Even Sen. Bob Corker, R-Tenn., who had been expected to vote against the bill over deficit concerns, has said he will support it. Sen. Thad Cochran, R-Miss. who was recently hospitalized, is expected to be available to vote for the bill. Sen. John McCain R-Ariz., who was also hospitalized has returned home but has said he will return here if his vote is needed.

The Bond Buyer

By Lynn Hume

December 18 2017, 4:57pm EST