Chicago’s attempt to clean up a legacy of wrong-way bets on interest rates is costing taxpayers at least $270 million since Moody’s Investors Service cut its rating to junk in May, city documents show.

The payouts to Wall Street banks, which come as the Windy City considers a record tax increase to cover pension costs, are more than the city spends a year to collect garbage at 613,000 homes, and could cover the cost of hiring more than 2,000 police officers. The pain isn’t over yet as officials plan another round of debt restructuring that could cost $110 million to unwind derivatives on its water debt early next year.

“I don’t think the public should be gambling with its funds,” said Richard Ciccarone, Chicago-based chief executive officer of Merritt Research Services, who has been analyzing municipal finance since the 1970s. “Save the speculation for people who risk their own money, not for taxpayers.”

The city was forced to restructure obligations after decades of failing to address its rising pensions and borrowing to cover debt service, a legacy that began under former Mayor Richard M. Daley and continued until this year under Mayor Rahm Emanuel. Moody’s downgrade of Chicago’s general-obligation debt in May forced the city to begin a debt restructuring the mayor was already planning.

Chicago and other municipal borrowers in the past decade made bets on the future direction of interest rates through agreements with banks to swap interest payments. But when rates fell under the Federal Reserve’s attempt to stimulate the economy after the financial crisis, many issuers ended up on the wrong side of the bets. Since then issuers have paid at least $5 billion to unwind the agreements.

Sewer Debt

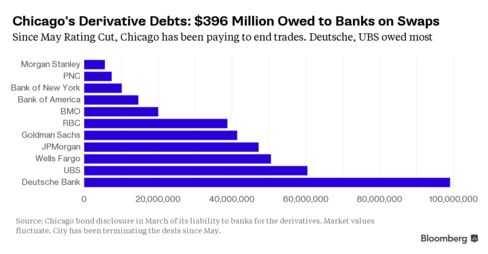

The city sold about $419 million of bonds Wednesday, part of which will cover $70.2 million to end an interest-rate swaps tied to variable-rate debt for the city’s sewer system. That’s on top of $185 million paid to unwind swaps on general-obligation and sales tax debt since May. The estimated $270 million total also includes the cost to banks and other professionals to restructure, according to data Bloomberg compiled from city documents. Chicago owed as much as $396 million to banks in March, before the city started terminating the swap agreements, according to market values at the time. Chicago paid less than mark-to-market valuations, said Molly Poppe, a city spokeswoman.

While the city’s refinancing and tax hike increase the burden on residents at a time when the city’s finances are already squeezed, investors and credit raters have praised the move. One month after cutting Chicago’s rating to speculative grade, Moody’s called the refinancing a “credit positive.” Now there’s more certainty about how much the city may have to pay out, Matt Butler, a Moody’s analyst in Chicago, said in a June 11 report.

Yields Decline

Chicago’s bonds has rallied since Emanuel pitched his plan to raise property levies by $588 million over four years. Federally tax-exempt bonds maturing in 2038 traded last week for an average of $1.04, up from $1.01 five weeks earlier, before the tax hike was announced. That trimmed the yield to 4.5 percent from 5 percent, according to data compiled by Bloomberg.

“It felt like the market was not comfortable with the amount of risk that we were taking,” Carole Brown, Chicago’s chief financial officer, said in an interview Monday. The restructuring “demonstrates kind of a conservative and responsible financial practice to eliminate that risk by eliminating those swaps.”

Wednesday’s deal will take care of the wastewater swaps, and the city will likely end the water-swap agreements in early 2016, according to Brown. Chicago will have to pay about $110 million to terminate the latter, according to the city.

About $332 million of the sewer issue is federally tax-exempt and was re-offered as fixed-rate obligations, and an additional $87 million of taxable debt will help cover the cost to terminate the agreements, according to bond documents.

A portion of federally tax-exempt securities due in January 2039 sold at a top yield of 4.4 percent, according to preliminary data compiled by Bloomberg. That’s about 1.5 percentage point more than 23-year benchmark municipal bonds. The taxable securities sold for as much as 6 percent yield, preliminary data compiled by Bloomberg show.

Borrowing Costs

The second-lien wastewater bonds, which are repaid from sewer-system revenue, won a higher rating from Standard & Poor’s this week, which raised its rating by one step to A, five levels above junk, and applauded the elimination of the liquidity risk. S&P has a stable outlook on the debt.

The wastewater credit faces “elevated volatility” because of its ties to the city, said Robert Amodeo, head of municipals for Western Asset Management Co., which has $452.5 billion under management, including some Chicago debt. He said he is considering buying the wastewater bonds given the strength of the underlying credit.

“There are some ongoing challenges there,” Amodeo said in a telephone interview from New York. “You can’t completely separate it from the city.”

The city’s ratings and borrowing costs are tied to its progress in getting the refinancing done, according to Brown. The hope is that credit companies will respond positively to the Emanuel administration’s steps to secure revenue for pensions, and eliminate the liquidity risk, leading to a higher rating and better borrowing costs, she said.

In the meantime, taxpayers in the city of 2.7 million are on the hook for the higher tab tied to deals made decades ago.

“We’re paying these fees at the same time the city is looking at the biggest tax increase in its history,” said Saqib Bhatti, a Chicago-based fellow at the Roosevelt Institute, which has been recommending that governments with swaps should push to cut the fees rather than pay Wall Street banks. “Working residents of the city are going to have to sacrifice for the city to pay these fees to the banks.”

Bloomberg News

by Elizabeth Campbell and Darrell Preston

October 13, 2015 — 9:00 PM PDT Updated on October 14, 2015 — 2:28 PM PDT