SUMMARY

- Investors may prefer premium municipal bonds once they separate fact from fiction.

- Yield to worst is a more meaningful metric than price to help determine value.

- A premium helps defend against punitive tax consequences of the IRS de minimis rule.

- Understanding premiums on municipal bonds can be confusing for many investors. Common misconceptions regarding premiums can prevent investors from making sound investing decisions in the municipal bond market.

Unfortunately, when it comes to premium municipal bonds, we often hear these fictions repeated:

- “If I buy a premium bond and it matures at par, I lose that premium. I will lose money, so I should avoid premium bonds.”

- “My muni bond, which yields 2% and pays a 5% coupon, provides me with income of 5%.”

- “If I buy a bond at $110 and it matures at par ($100), I get to book a $10 loss.”

The concept of “lost premium” is a fiction. In this Insight, we present facts about premium municipal bonds in order to help dispel common misconceptions. We explain why most municipal issuance comes as a premium, how the coupon factors into the equation, why the yield to worst (YTW) is so important to consider, and how the investor can opt to preserve the premium paid on a municipal investment.

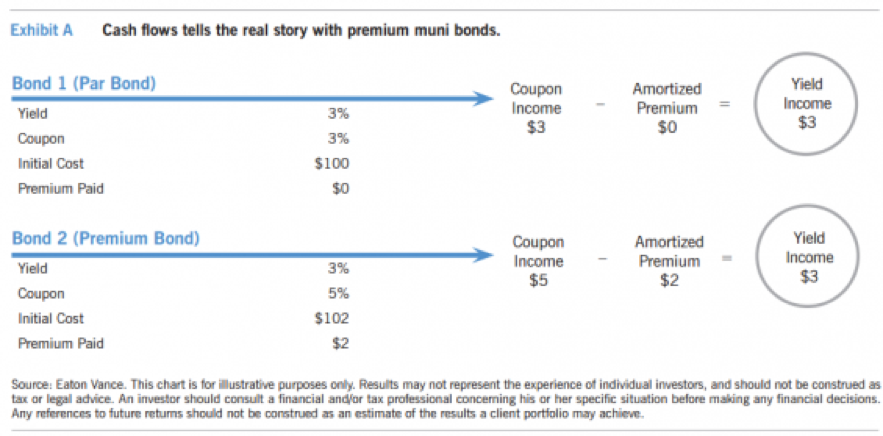

Fact #1: The size of a bond’s premium is not an indication of value.

Put differently, a premium bond is not inherently an overvalued bond. Historically, the size of a bond’s premium is directly related to the bond’s coupon – the higher the coupon, the higher the premium. This is best explained by comparing two bonds and their associated cash flows.

Consider two bonds that both mature in one year, shown in Exhibit A. Both bonds have a YTW of 3%; YTW is a measure of what investors earn on their money, expressed as an annual rate. Which bond do you prefer, and why?

At maturity in one year, the cash flows associated with each bond tell us the real story. Netting the coupon income against the amortized premium is how the investor determines the true income (or yield income) of a municipal bond. Both scenarios assume the buyer receives $100 par back at maturity; both bonds provide a return of 3% despite one having a premium and one not having a premium.

Importantly, there is no loss on either bond; this dispels one of the most oft-repeated fictions about premium municipal bonds. The premium on Bond 2 is amortized down and is returned in the form of a higher coupon; it is not being lost.

Fact #2: Yield to worst is the best determinant of value for premium municipal bonds.

The price of a premium bond is certainly relevant, but it must be viewed in the context of the bond’s other characteristics, such as the coupon rate, call and put provisions, time to maturity and YTW, as well as other factors such as credit structure and the availability of alternatives offering similar income potential.

Many investors confuse coupon and yield (more precisely, yield to worst or YTW). Yield is defined as what you earn on your money. As outlined above, when you net the annual coupon income against the amortized premium, the net result is the yield income of the bond. This is the math behind municipal bonds and it always holds true.

Yield, therefore, is a more meaningful metric than price to help investors to determine the value of a particular bond issue, and YTW factors in the possibility of a bond issue potentially being called or subjected to default or other provisions.

The fact that investors receive 1099-INTs with only the coupon income can be misleading. Investors must determine the bond price amortization (mistakenly thought of as lost premium) for the year and subtract that from the coupon income for their tax filings. The bond amortization schedule is readily available. It is this net number (coupon income minus bond amortization) that must be reported on the investor’s annual tax return.

Fact #3: Municipal bonds issued with a premium guard against tax consequences of de minimis risk.

Bonds are issued with premiums in the municipal market to guard against a taxable event resulting from the IRS de minimis rule. Only issuers can create tax-exempt income. When market conditions dictate that a bond should sell at a discount, accretion from the discounted price may represent income taxed as ordinary income instead of capital gains. Per the IRS, a discount (from the lower of par or an accreted original issue discount) equal to 0.25% times the number of full years to maturity is considered inconsequential (or de minimis). Once the discount exceeds this threshold however, all accretion is taxable as ordinary income.

Here, an example might help better explain the concept. Take a bond with a 20-year final maturity issued at $100, but purchased in the secondary below $95. As the bond accretes or gains value (it will mature at $100, or par), the accretion is subject to being taxed as ordinary income.

It is because of this IRS rule that investors in the muni bond market demand high premiums, also known as coupon protection. A stated coupon in excess of the YTW of a bond means its price will be at a premium, offering some protection against potential higher taxes.

We note that in 2015, roughly 75% of bonds issued in the market had 5% or greater coupons with significant price premiums. In addition, the publicly disclosed muni trade history on the website of the Municipal Securities Rulemaking Board (MSRB) shows a large majority of trades with prices of $115 and higher, indicating the prevalence of bonds offering coupon protection.

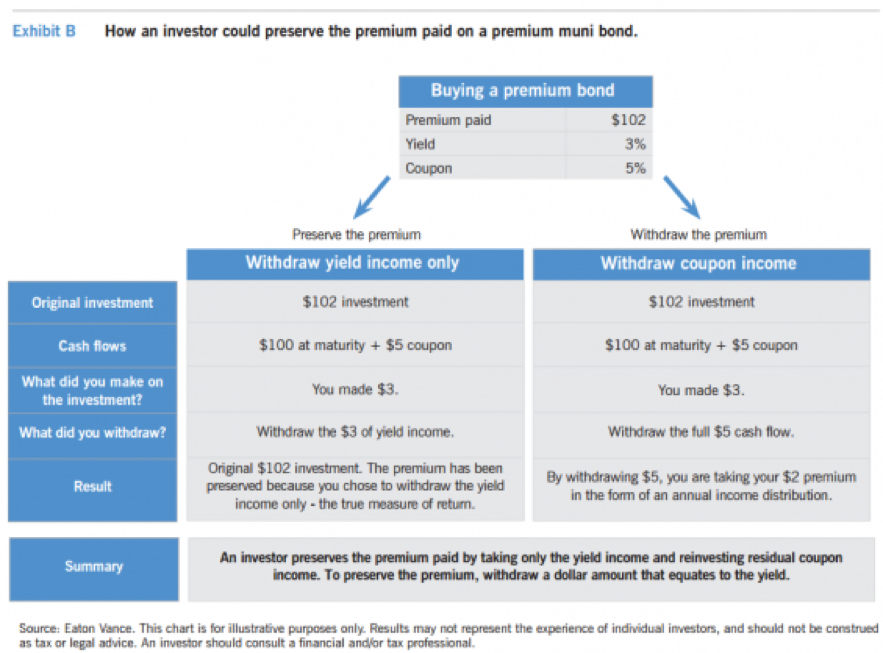

Fact #4: An investor can preserve the premium of a bond by only receiving yield income instead of the full coupon income.

As discussed, municipal bonds are issued at premium prices to guard against taxes. The higher the premium, the higher the coupon rate on the bond. But as also discussed, the true measure of bond return is only the yield, not the coupon. It is important to realize that taking an income distribution in excess of the yield means you are eroding the principal of your muni bond investment. If a bond yields 3% and the coupon rate is 5%, receiving a distribution of 3% preserves the premium paid, while receiving a distribution of 5% erodes the premium. A premium bond amortizes some of its premium every year, reducing the cost basis until the bond matures at par. This amortizing premium is directly offset by the coupon income in excess of the yield. An investor wishing to preserve the premium paid can opt to take only the income corresponding to the yield, or yield income, and, in doing so, preserve the original premium paid.

Consider a premium bond with one year to maturity, a coupon of 5% and a yield of 3% purchased at a premium price of $102. In the first case, the investor chooses to receive the full coupon income of 5% as a distribution, as shown in Exhibit B.

Alternatively, if the investor had instead chosen to take a distribution of only the yield income of 3% (the true measure of return), residual coupon income of 2% would have been realized. (You can determine the excess coupon income by subtracting the yield from coupon. In this case, it’s 5% – 3% = 2%) By taking only the yield income and reinvesting the residual coupon income, the investor preserves the premium paid.

Why we favor premium bonds

Investors tend to prefer premium municipal bonds once they separate fact from fiction. Fortunately, the facts are easy to understand:

- The size of a bond’s premium has nothing to do with the bond’s value.

- Yield is the meaningful metric – not price – to help determine the true return.

- Premiums help defend against punitive tax consequences of the de minimis rule.

- An investor can preserve a premium paid by taking only yield income.

For savvy investors, premium bonds can be an appropriate vehicle for building a muni bond portfolio with a defensive structure in today’s low-yield environment. All else equal, a premium bond (higher coupon) will likely outperform a par bond in a rising rate environment thanks to a lower duration, or sensitivity to interest rates.

Relying on YTW is just one of the many factors to consider when purchasing premium bonds. We believe security selection will be critical to success when investing in a market as vast and increasingly complex as the municipal bond market. We believe relative value analysis is just as important. As always, individual investors may benefit from skilled professional management and credit research.

Importance tax considerations

Many investors are not aware of IRS guidelines on reporting tax-exempt investment income, which instruct investors to report on line 8b of the 1040. This is not the 1099-INT income, but rather the income less the annual reduction (or, more accurately, the amortization) of bond premium.

Though provided by the advisor’s firm, investors can calculate the premium amortization (or reduction of premium) themselves. The IRS instructs investors to use the current yield method of amortizing bond premium.

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. A portion of municipal bond income may be subject to alternative minimum tax. Income may be subject to state and local tax.

The views expressed in this Insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

May 2, 2016

by Jonathan Rocafort, Christopher Harshman, Evan Rourke

of Eaton Vance

©2016 Eaton Vance Distributors, Inc. • Member FINRA/SIPC Two International Place, Boston, MA 02110 • 800.836.2414 • eatonvance.com