Taylor Riggs, a contributor to Bloomberg Briefs, talks with reporter Amanda Albright about this week’s municipal market news.

Watch the video.

Bloomberg Briefs

October 13, 2016

Taylor Riggs, a contributor to Bloomberg Briefs, talks with reporter Amanda Albright about this week’s municipal market news.

Watch the video.

Bloomberg Briefs

October 13, 2016

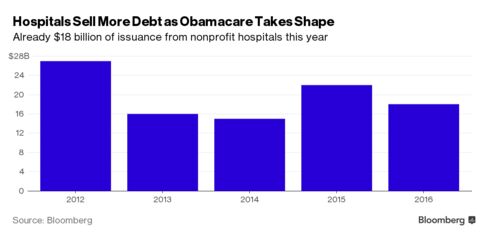

NEW YORK — In July, investors gobbled up $1 billion of bonds from a financially-strapped Catholic hospital system in Illinois called Presence Health Network, even though it offered few contractual guarantees debt buyers typically require.

The deal, rated just above junk status, is emblematic of a fever that has swept the $3.7 trillion U.S. municipal bond market: yield-chasing investors not only piling into riskier debt, but also increasingly willing to accept less protection in the event of a default.

Some portfolio managers say it has been a decade since they have seen such a strong seller’s market.

“It’s reminiscent of right before the Great Recession, where there was a long period where high-yield rates were low and demand was high,” said William Black, senior portfolio manager for the City National Rochdale Municipal High Income Fund.

Low and negative sovereign interest rates have contributed to a scramble for relatively higher yielding U.S. municipal debt. Foreign buyers now hold more muni bonds than ever, U.S. Federal Reserve data show.

Overall, investors have poured nearly $10 billion into high-yield municipal bond funds so far this year, according to data from Lipper, a Thomson Reuters unit. That is more than any other full year in nearly the last quarter century except 2006, which had $10.1 billion of inflows. (Graphic: http://tmsnrt.rs/2dylqFl)

Taking advantage of the seemingly insatiable demand, some borrowers are offering weaker or fewer guarantees, so-called covenants, such as debt reserve funds and debt service coverage ratios.

Because they are based on many factors, credit ratings alone may not reflect the quality of covenants, so some investors may be taking on greater risks than they realize.

Such “covenant light” bonds were harder to offload after the market tumbled in late 2008, while investors who held them saw valuations swing wildly because of infrequent trading and huge price gaps, analysts said.

“Some funds got just clubbed. That was frankly very traumatic for a lot of investors, and fund managers too,” said Joseph Krist, partner at the Brooklyn-based public finance consulting firm Court Street Group.

In a default, workouts are harder. Covenant light bondholders have fewer tools to intervene, for example by requiring issuers to hire turnaround professionals or take other corrective action earlier. They also risk deeper losses in bankruptcy than those with greater protection.

HEALTHCARE AND CHARTER SCHOOLS

Sectors such as healthcare, charter schools, and senior living facilities tend to be more prevalent covenant light issuers, in part because they may struggle more to generate consistent operating margins.

Hospitals and charter schools issued 44 percent and 76 percent more debt by par amount so far this year, respectively, compared with 2015, Thomson Reuters data show. Senior living facility issuance rose 6 percent.

They come in other sectors too. The city of San Antonio, Texas, sold AA-rated junior lien water system bonds on Thursday without a reserve fund – a fact disclosed in the title of the bond documents.

But many covenant light deals are unrated or speculative grade. Issuers have sold more than 400 percent more bonds rated junk at BB and BB- by S&P Global Ratings so far this year than last year, Thomson Reuters data show.

One such example is Summit Academy North, a junk-rated Michigan charter school that missed deadlines for annual financial data in four of the last five fiscal years, according to bond disclosures.

Summit sold $22.5 million of refunding bonds on Aug. 31 with a cash on hand liquidity threshold of just 30 days, a very low level for the sector.

Even so, the top yield was just 4.75 percent on 2035 bonds – a rate that an investment-grade borrower would have likely offered only a couple of years ago.

“I cannot believe some of the deals that are getting done in the muni market right now – without a mortgage, low debt service reserve fund,” Mark Paris, head of municipal portfolio management at fund manager Invesco, said at a recent event.

Some funds say they have little choice but accept fewer safeguards in order to put clients’ cash to work.

“Money is coming in to the point where people have to buy something,” said one market professional who declined to be named.

Institutional investors have pushed back by demanding greater liquidity covenants, said Mark Taylor, a portfolio manager and head of high-yield research at Alpine Woods Capital Investors.

By September, he had a stack of rejected deals in his office that was four-feet tall, Taylor said. Nonetheless, the deals he has turned down are getting picked up by others.

“There is a plethora of deals coming to market that people probably would have rejected nine months ago.”

By REUTERS

OCT. 11, 2016, 1:03 A.M. E.D.T.

(Reporting by Hilary Russ; Editing by Daniel Bases and Tomasz Janowski)

NEW YORK — The great bull run for the municipal-bond market may be running out of juice.

For the past year, bonds issued by state and local governments have been red-hot investments. Muni-bond mutual funds have had 53 straight weeks of inflows, according to the Investment Company Institute. That’s one of the longest streaks on record, and they attracted cash at the same time that investors were leaving stock mutual funds. Even Puerto Rico’s default on its debt and Britain’s vote to exit the European Union, which roiled bond markets worldwide earlier this year, didn’t interrupt the muni market’s trajectory.

“Munis have been the darling asset class of the past two or three years,” says Chris Alwine, head of the municipal group at Vanguard.

Now there are signs that this long bull run may be coming to an end. After 10 straight months of positive monthly returns, the iShares National Muni Bond exchange-traded fund, the largest muni ETF by assets, posted a very narrow loss in July. While returns were positive in August, the fund lost about 0.6 percent in September and is on track for another loss in October.

Munis have always appealed to U.S. investors, who are attracted to their reputation for safety and the fact that their income is free of federal income taxes. It’s an incentive offered to get investors to lend to local government so they can build schools, highways and sewer systems. In some cases, income from muni bonds is also free from state or local income taxes.

Over the past 12 months, the iShares ETF has returned 4.3 percent. That beats the returns for the largest bond mutual fund, Vanguard’s Total Bond Market Index fund, which returned a nearly identical amount, after taking into account the tax savings.

In the past couple of years, low interest rates around the world and a volatile stock market have also driven investors from outside the United States into the municipal-bond market, even though non-U.S. residents don’t get the tax advantages.

Given how high prices for muni bonds have moved, some fund managers say that a pullback is inevitable. The 10-year yield on the AP Municipal Bond index, which moves inversely to bond prices, hit a low of 1.69 percent in July and has been climbing ever since. It ended last week at 1.878 percent. Even the relatively small increase in yields has put downward pressure on prices of municipal bonds, says James Kochan, chief fixed-income strategist at Wells Fargo Funds Management.

If many of the recent muni buyers have been coming with the intent of avoiding turmoil elsewhere in the bond world, a few months of negative returns for munis could spark a sell-off.

It wouldn’t be the first time that investors in munis, a historically sleepy market, have been spooked in recent years. The most recent case was in the 2013 “taper tantrum,” when investors became anxious about the possibility of an upcoming interest-rate increase. When investors dumped muni bonds during that episode, prices quickly dropped. The iShares ETF lost 8 percent in just four months.

“I think some investors are taking more risk than they are aware of,” says Chris Ryon, portfolio manager at Thornburg, who co-manages one of the largest muni bond funds.

Given the uncertainty, investors who hold munis should be looking to pare back on risk, says Ryon, who suggests sticking with higher-quality muni offerings, especially because lower-rated muni bonds aren’t offering that much more income than higher-quality muni bonds. In the parlance of bond investors, the “spread” is not that wide.

With that said, there’s no need to ditch high-yield munis entirely, says Peter Hayes, head of the municipal bonds group at BlackRock. “For the rest of the year, we think returns will be largely generated by income,” he says. “That means you need to own some amount of high-yield.”

Investors should also shorten the duration, or maturity, of their holdings, says Wells Fargo’s Kochan, because prices of longer-term bonds tend to fall more when interest rates rise.

Hayes says he favors 15-year maturities, which he calls the “sweet spot.” The good news for investors: With global interest rates still extremely low and the credit quality of munis generally stable, most experts view the recent dip as a pullback, not the start of a bear market.

Says Hayes: “The past month has created a little bit of better buying opportunity.”

By THE ASSOCIATED PRESS

OCT. 13, 2016, 12:39 P.M. E.D.T.

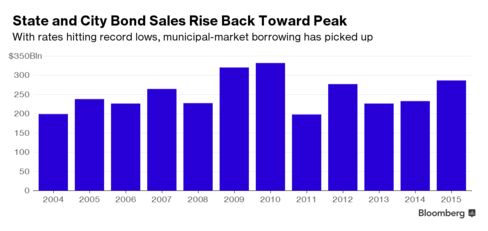

Municipal bond issuance for September swelled 45% to $35.7 billion, the highest volume for the month in records going back to 1986, driven by an unexpected surge in new money deals.

The total par amount of the month’s 980 sales surpassed the previous September volume record set in 2010, when $35.6 billion of bonds were sold. Through three quarters, the market has produced $334 billion of issuance in 10,046 deals, according to data from Thomson Reuters, on pace to surpass the $400 billion mark. At this time last year volume totaled $319.4 billion in 10,359 deals.

The largest recorded issuance year was 2010, when the volume hit $433.27 billion.

“It certainly seems likely given that October should also be heavy, with more than $14 billion next week. We had [estimated] $400 billion with a possible upside surprise and it seems the surprise might actually be happening,” Mikhail Foux, director of research at Barclays Capital, said Friday.

Foux said new money deals have been the biggest surprise.

“Who would have thought that after such a slow first quarter, we are likely going to surpass last year’s number, which one of the largest ever years in terms of issuance,” he said. “A pickup in new money is the biggest story of 2016 and likely going forward. It seems that we are finally starting to address our infrastructure needs. There was a lot more issuance from the transportation sector and there is more than $200 billion of bond deals on ballots.”

For the third quarter alone, there were $109.7 billion of deals in 3,131 transactions, up from the $92.6 billion in 2,951 transactions during the third quarter of 2015.

“The sheer amount of issuance has been pretty impressive. I think the hope is that the amount of supply puts some pressure on the yields and creates a backup, which would be welcomed,” said Dawn Mangerson, managing director and senior portfolio manager at McDonnell Investment Management. “We said issuance wouldn’t wane, and we were right. We are looking good right now; we should see a decent calendar throughout the rest of the year.”

Though volume was up the past two months and third-quarter issuance increased year-over-year, volume for the three months was down from the second quarter.

“The volume hasn’t reached a point where it was too much for the market to absorb,” Mangerson said. “It has been surprising how much consistent high demand for munis we have seen all year long and also that we didn’t see any volatility this month.”

Mangerson said volume could slip toward the end of the year, when and if the Federal Open Market Committee decides to raise rates.

“The second quarter is typically the heaviest; we had a substantial slowdown in July – partially due to Brexit- but supply picked up in August and September,” Foux said, referring to the British vote to leave the European Union.

For the month, new money deals catapulted nearly 68% to $16.99 billion in 470 issues, from $22.21 billion in 799 issues during the same period last year.

Refundings, which have been strong for most of the year due to persistent low interest rates, were up 19% to $12.19 billion in 423 transactions from $10.23 billion in 353 transactions during September of last year.

Combined new-money and refunding issuance rose by 54.6% to $6.51 billion from $4.21 billion.

Negotiated deals were higher by 57.7 % to $27 billion, while competitive sales increased by 58.6% to $7.61 billion from $4.79 billion.

Issuance of revenue bonds increased 82.2% to $26.65 billion, while general obligation bond sales were down 9.1% to $9.05 billion.

Taxable bond volume increased 32.8% to $2.13 billion, while tax-exempt issuance increased by 45.2% to $32.25 billion.

Minimum tax bonds issuance gained to $1.32 million from $760 million.

Private placements sank to $1.09 billion from $2.66 billion.

Zero coupon bonds more than doubled to $360 million from $132 million.

Bond insurance increased 26% for the month, as the volume of deals wrapped with insurance rose to $1.84 billion in 140 deals from $1.46 billion in 117 deals.

Variable-rate short put bonds gained 7.7% to $1.06 billion from $986 million. Variable-rate long or no put bonds jumped to $734 million from $31 million.

“This is probably due to all the SIFMA related concerns, much higher SIFMA and libor rates are making issuing floating rate notes more costly,” said Foux.

Bank qualified bonds improved 6.4% to $1.59 billion from $1.49 billion.

Seven out of the 10 sectors saw year-over-year gains. Health care more than doubled to $5.69 billion from $1.67 billion, utilities also more than doubled to $3.32 billion from $1.36 billion, general purpose increased 34.6% to $8.44 billion from $6.27 billion, housing rose to $2.16 billion from $943 million, health care increased to $5.69 billion to $1.66 billion, environmental facilities climbed to $379 million from $76 million and electric power went up to $1.83 billion from $516 million.

On the other end of the spectrum, the education sector was barely down to $7.17 billion from $7.20 billion, development dropped 15.9% to $729 million and public facilities were down to $932 million from $1.04 billion.

As for the different types of entities that issue bonds, five were in the green: state governments, state agencies, counties and parishes, cities and towns and districts.

One other thing that Foux noted was that in general, issuers tried to bring deals before FOMC announcements, not just this month but in general.

“It seems that we see more pension obligation bonds, as issuers are trying to plug the pension funding gap.”

California is still the top state for issuance for the year to date, followed by Texas, New York, Pennsylvania and Florida. These numbers encompass all of the individual issuers within the state.

Golden State issuers this year have sold $47.53 billion, with the Lone Star State in second with $41.55 billion. The Empire State follows with $35.36 billion. The Keystone State is in fourth with $15.24 billion and The Sunshine State rounds out the top five with $15.08 billion.

“October could be solid as issuers could try to bring deals before the elections,” Foux said. “November and December should be lighter, though we have some uncertainty related to the December FOMC and issuers might try to pull deals from January to get in front of it.”

The Bond Buyer

By Aaron Weitzman

September 30, 2016

Regardless of which candidate takes the oath of office next January, improving our country’s infrastructure will be on the next President’s agenda.

An Association of Equipment Manufacturers poll shows that over 70% of Americans want government to address our growing infrastructure crisis.

Turning that into reality will require a clear understanding that the need for additional investment is real.

Members of Congress, governors and mayors from across the country have advanced bipartisan solutions to broadly address this critical need. So too has the financial services sector that works with federal, state and local governments to raise capital crucial to infrastructure investment.

Nevertheless, the level of investment by government and the private sector falls short of meeting the nation’s current and future infrastructure needs, and the central question remains how to pay for it.

We need to do more with existing resources while not losing sight of the crucial need for more investment to pay for infrastructure needs. While others attempt to address the political challenge of identifying more sources of infrastructure funding, we can work toward implementing a few tangible policy ideas.

Two ways for state and local governments to achieve more with existing resources is by encouraging broader use of a construction procurement method called design-build and treating infrastructure as assets.

The traditional approach to project procurement is known as “design-bid-build,” a multi-step process that separates the design and construction functions. Design-build simplifies the process by making a single entity responsible for both and collapses the procurement into one step, saving time and delivering a better, more cost effective result.

In New York, the NYU Rudin Center for Transportation and Citizens Budget Commission completed studies projecting design-build savings of up to 20% compared with traditional methods. However, design-build is still not broadly available for public infrastructure projects in all 50 states.

State and local government should also treat infrastructure as assets through better tracking and disclosure of on-going costs. The benefits are two-fold: a healthier understanding of the true ongoing costs and greater transparency will lead to more private sector involvement.

Identifying non-essential assets that can be auctioned to the private sector and put to productive use can create new revenue for government without affecting its core mission, a win-win scenario.

Three quarters of annual infrastructure spending in the U.S. is funded through the $3.7 trillion municipal bond market, where private investors purchase tax-exempt bonds issued by state and local governments.

The key advantage of municipal bonds is that interest on them is exempt from federal and state income taxes. This means investors will accept a lower interest rate, providing state and local governments with the benefit of borrowing money at the lowest interest rate available to anyone financing infrastructure, including the U.S. Treasury. This also allows state and local governments to raise capital up front to fund long use projects like airports, roads and bridges and amortize the cost over the life of the project.

The next administration should avoid calls to curb the use of tax-exempt bonds and rather seek to create a more certain tax and regulatory environment expanding the use and easing the availability of lower cost municipal debt for public-private partnership (P3) projects that involve a government entity.

Our economic competitors are using P3s as a way to capture private sector efficiencies while providing public infrastructure and retaining government ownership.

Making tax-exempt financing available for P3 projects would allow the two models to converge, leaving state and local governments with the best of both – access to the lowest cost financing available and private sector efficiencies.

The Move America Act, bipartisan legislation sponsored by Senators Ron Wyden (D-OR) and John Hoeven (R-ND), would authorize Move America Bonds, a new category of tax-exempt bonds that would be exempt from most private use restrictions, as long as the facilities are available for public use.

Providing tax incentives for investment in targeted sectors has been an effective in low income housing development and more recently renewable energy production. The Move America Act would provide for a limited, targeted tax credit applicable to equity investments in infrastructure, and Congress should consider such an idea.

The next president and Congress should embrace these ideas and spur a new chapter of infrastructure revitalization that will strengthen our economic future.

The Bond Buyer

By Kenneth E. Bentsen, Jr., and Chris Hamel

September 26, 2016

Kenneth E. Bentsen Jr. is president and CEO of the Securities Industry and Financial Markets Association. Chris Hamel is head of Municipal Finance at RBC Capital Markets and chair of SIFMA’s Infrastructure Policy Committee.

WASHINGTON – Infrastructure projects in the U.S. are plagued by long pre-construction periods, an under-utilization of the public-private partnership financing model, and an inability to both gain public support and access capital, a panel of market participants said this week.

The four-member panel at the Securities Industry and Financial Markets Association’s annual conference here on Tuesday, entitled “Financing Infrastructure for the 21st Century,” discussed ways in which P3s could be used in order to improve roads, bridges and other struggling areas in a more effective manner.

Chris Hamel, the moderator of the panel and the managing director and head of the municipal finance group for RBC Capital Markets, said the panel’s goal was to foster a discussion on solutions rather than the underlying problems. He stressed the advantageous features of the $3.7 trillion muni market that allows for borrowing at a cost lower than Treasury rates.

The panel estimated that the U.S. is in need of $3.6 trillion of infrastructure investments by 2020, and cited a recent study that found 70% of Americans want governments at all levels to do more about infrastructure.

“We need to capture what is unique about our tax exemption and our highly decentralized government structure and combine it with the effectiveness of the private sector,” Hamel said.

“It is going to come from a collaboration of people with multiple levels of expertise.”

Several of the panel members, including Geoffrey Chatas, senior vice president and chief financial officer for Ohio State University, gave examples of how private help has been used effectively to expedite projects and help in their management after construction.

Chatas cited how his school’s airport, seven hospitals, set of energy assets and parking garages have been made possible by using the expertise of private entities. Ohio State is not shying from issuing debt, he said, adding that the school has had $3.5 billion in issuances over the last 20 years, while higher education costs have quadrupled.

The $483 million upfront payment for a 50-year lease for a campus parking lot in 2012 has allowed for an endowment distribution of $105 million over the past four-and-a-half years, he said. Those funds have been allocated toward an arts district, a campus bus system, student scholarships and faculty hirings.

Chatas said there have been “outstanding” financial results, although he did admit growing pains in managing some of the parking facilities during the culture change.

“We’re trying to think very differently,” Chatas said. “Let’s bring in partners, let them raise the capital and then manage the properties. Let us focus on teaching and learning.”

Tyler Duvall, a partner at McKinsey & Company in Washington, said that the pre-construction process for national infrastructure projects is “a major problem,” one that can often take between 40-60 months. This is often due to complex disclosure mechanisms around the environmental review process, leading to more discussions than decisions, he said.

There is no federal government entity that currently exists to accelerate both this process as well as a more effective revenue stream once construction begins. He suggested the federal government create one to have someone accountable for the end-to-end process and put the U.S. more on a par with Canada and Australia in terms of their infrastructure success.

The federal government has also been plagued by a lack of a problem statement in the highway area, he added.

“The capital is there and it’s cheaper than ever,” Duvall said. “That’s not the issue. Connecting the capital with projects is the issue.”

Suzanne Shank, chairwoman and CEO of Siebert Cisneros Shank & Co., a municipal investment bank based in New York City and Oakland, Calif., agreed Tuesday that the U.S. has some catching up to do with other countries.

“We’re not making headway and the gap is growing,” she said.

Duvall said the U.S. has “phenomenal” lending programs that need to be tweaked to create better revenue streams, a task he said can be done administratively without legislation.

“It’s all about prioritization,” he said.

Another successful P3 cited by the panel was the $4 billion renovation of LaGuardia Airport in New York, which began in June. Francis Sacr, managing director of infrastructure and transportation project finance for Societe Generale, the corporate and investment bank that served as the financial advisor to LaGuardia Gateway Partners, said it proved complicated because of the multiple financers involved.

Sacr said the project to renovate the dilapidated airport used $1 billion of passenger facility charge revenues from the Port Authority of New York and New Jersey as well as $2.5 billion from special facilities bonds and up to $500 million in taxable delayed-draw private placement bonds.

As the largest airport financing deal ever done in the U.S., the P3 structure proved especially beneficial because of the cost overruns, he said.

“Finding multiple sources of capital was the most important part of the solution,” Sacr said.

On a macro level, Sacr said an underinvestment in U.S. infrastructure comes partially as a result of what he feels is shortsightedness.

“Infrastructure is a long-term investment, while politics is a short-term focus,” Sacr said. “It really does require a long-term vision from the governments involved.”

The Bond Buyer

By Evan Fallor

September 28, 2016

PHOENIX – The DC Water and Sewer Authority closed on a historic deal Thursday, issuing the nation’s first Environmental Impact Bond (EIB) to fund the initial green infrastructure project in its DC Clean Rivers Project.

The $25 million, tax-exempt EIB was sold in a private placement to the Goldman Sachs Urban Investment Group and Calvert Foundation, netting DC Water a 3.43% interest rate that is comparable on a cost of funds basis to its historic cost.

The proceeds of the bond will be used to construct green infrastructure to absorb and slow surges of stormwater during periods of heavy rainfall, preventing an overflow of untreated sewage (known as a combined sewer overflow, or CSO) into the Potomac and Anacostia Rivers or their tributaries. The green infrastructure includes absorbent materials and gardens that mimic natural rain absorption processes.

The EIB allows DC Water to attract investment in green infrastructure through an innovative financing technique whereby the costs of installing the green infrastructure are paid for by DC Water, while the performance risk of the green infrastructure in managing stormwater runoff is shared among DC Water and the investors. As a result, payments on the EIB may vary based on the proven success of the environmental intervention as measured by a scientific evaluation of the results.

The structure of the deal includes three “tiers” of performance depending on how well the green infrastructure controls the runoff.

The investors will receive interest payments as typical for bondholders. Depending on the results, an additional payment may be due on the bonds’ mandatory tender date of April 1 2021.

If runoff reduction is greater than 41.3%, a “tier 1” outcome, the investors will receive from DC Water an “outcome payment” of $3 million. In a tier 2 outcome where runoff reduction is 18.6% or better but less than 41.3%, the investors will be due only their normal principal and interest.

In a failed tier 3 outcome where runoff reduction is less than 18.6%, the investors will owe DC Water a “risk share” payment of $3.3 million that the trustee will then factor into future payments. That would net the investors a roughly 0.5% return, and DC Water would abandon green infrastructure for traditional tunnels or “gray” infrastructure.

“This environmental impact bond represents the first time that DC Water has explicitly tied financial payments to environmental outcomes, in this case reducing stormwater runoff, which causes the CSOs that pollute the District’s waterways,” said DC Water chief financial officer Mark Kim.

Kim said the EIB is on DC Water’s subordinate lien, on par with the majority of its debt. DC Water is a regional water authority that provides services to the District of Columbia, as well as to parts of Maryland and Virginia.

“This unique bond offering is the result of DC Water’s relentless commitment to innovate and pursue every available avenue to provide the best service at the best price to our customers and to the greater community we serve,” said chief executive officer and general manager George S. Hawkins.

Kim said that a tier 2 result is thought to be most likely, and that DC Water and its nontraditional muni investors were willing to make a bet together that green infrastructure would be successful.

“We’re thrilled to partner with DC Water to help pioneer this innovative financing mechanism that will not only benefit the community environmentally, but also stimulate local job creation,” said Margaret Anadu, Goldman Sachs managing director who leads the Urban Investment Group. “This first ever environmental impact bond will finance the construction of green infrastructure and support economic development in the District.”

Beth Bafford, investments director for Bethesda, Md. based nonprofit Calvert Foundation said the foundation was excited to test how effective the green infrastructure would be and noted its potential as a national precedent for water utilities.

“This work is critical for residents in our hometown and has national implications for how to finance green infrastructure solutions to combat the effects of extreme weather on aged, vulnerable sewer systems,” Bafford said.

The White House also commented on the potential of the unique deal to create a model for other issuers. The project’s development was aided by a federal Social Innovation Fund Pay For Success Grant.

“In launching a project that is the first of its kind in the nation, DC Water has opened the door for others to follow their example,” said Dave Wilkinson, director of the White House Office of Social Innovation.

Public Financial Management is financial advisor for the deal, with Squire Patton Boggs as bond counsel and the Harvard Kennedy School Government Performance Lab providing technical advice. Quantified Ventures was the Pay for Success transaction coordinator, and Orrick, Herrington & Sutcliffe is investors’ counsel.

The Bond Buyer

By Kyle Glazier

September 29, 2016

Mayor Sylvester Turner is garnering praise for his proposal’s comprehensiveness and balance.

Earlier this month, Houston Mayor Sylvester Turner released his outline for fixing the city’s underfunded pension system, an issue that earned the city a credit rating downgrade in March.

Observers say the plan is the best effort yet at solving a problem that has eluded past city officials. If approved, the proposal would immediately cut Houston’s unfunded liability by $3.5 billion — or nearly in half — while putting Houston on a path to pay off the rest of its pension debt over the next generation.

The proposal has several moving parts, including concessions from city workers, a requirement that the city make its payments going forward and a change in some accounting assumptions as a way of making the system less exposed to the risks of the financial market. It also calls for issuing pension obligation bonds to help plug the funding hole.

What makes the effort even more remarkable is that Turner is less than a year into his first term. But Turner is no ordinary first term mayor.

Prior to being elected, he had already spent 25 years serving a portion of the Houston metro area in the state legislature. It’s his experience and the connections he’s made, both politically and in the business community, that Turner will draw on when he takes the proposal to the city council in early October. The state legislature ultimately has final approval on any changes to the pension system, but most believe that Turner will encounter little resistance there.

“The number one thing is the relationships Mayor Turner has,” said city finance director Kelly Dowe, whom Turner kept on from the previous administration. “When he says, ‘Folks, this isn’t sustainable,’ it’s different from someone else saying it.”

Indeed, Turner’s proposal appears to strike the right amount of give-and-take that’s required for all parties to get on board. First, the city is stepping up in terms of accountability, meaning it would be required to make its pension payment annually.

What’s more, the system would immediately incorporate a more realistic investment rate of return assumption in valuing its pension liabilities. Currently, Houston is an outlier among public plans and assumes its investments will earn 8 or 8.5 percent annually. That’s much higher than the national average of plans and even higher than Houston’s recent investment experience. Turner’s proposal assumes a 7 percent rate of return, which is lower than the national average and bumps up Houston’s total liabilities to a more realistic $7.7 billion (from under $4 billion as reported).

The pension plans would also switch from an open amortization period — which is like refinancing your home every year and never paying off the loan — to a closed one. That change puts the city on a path to fully pay off its pension debt over 30 years.

In terms of employee concessions, Turner is deftly leaving it up to the unions. At a press conference announcing the reform, he said the three plans in the pension system had identified a collective $2.5 billion in cuts. While not specific, that will likely mean some combination of cuts to retirees’ cost-of-living adjustments and their deferred retirement option plans benefits, which allow retirement-age employees to keep earning retirement benefits as they continue to work.

The planned issuance of pension obligation bonds would infuse another $1 billion into the system, bringing down the total unfunded liability to about $4.2 billion. Issuing bonds to plug pension funding holes can be controversial because it doesn’t eliminate debt, it simply moves it from a pension system’s balance sheets to the city’s debt ledger.

City Controller Chris Brown said at a discussion last week hosted by Rice University’s Kinder Institute that he is typically skeptical of issuing pension obligation bonds. But he added he would support the idea as long as the city doesn’t use the bonds as a replacement for making its annual payments and if Houston receives a favorable interest rate on the bonds.

Notably, Turner’s proposal doesn’t call for a new tax as has often been done in other places — such as Chicago — as a way to get a poorly funded pension plan back to health. That aspect has pleased the business community, which has said it wants the city to get its pension costs under control before discussing taxes. But Turner does plan to ask city voters next year to lift Houston’s 12-year-old revenue cap to help reinvest in needed infrastructure and parks projects.

So far, the Houston Municipal Employees Pension System and the Houston Police Officers’ Pension System have signed on to the mayor’s plan. That leaves the Houston Firefighters’ Relief and Retirement Fund, which has yet to endorse Turner’s proposal. The firefighters’ plan is directly controlled by the legislature. That means if they don’t sign on to the reform, they risk “the horrendous challenge” of the legislature making changes to their plan, said Max Patterson, the executive director of the Texas Association of Public Employee Retirement Systems.

“Generally speaking, [employees] should be happy with this,” he said at last week’s event. “Because you have to measure it against the other side of, if I don’t get this, what will I get?”

GOVERNING.COM

BY LIZ FARMER | SEPTEMBER 29, 2016

For years there have been voices writing, speaking and worrying about U.S. unfunded pension liabilities. I, for one, included. Never should investors ever buy pension obligation municipal bonds. Cities, states and counties issue POBs because their pensions are grotesquely under water and they cannot meet their liabilities. The reasons are long, but pretty simple: Poor investment results; demographic shifts due to people living longer; mismanagement; devastating union-negotiated wage and benefit increases; low retirement age; and unrealistic assumed rates of return on assets.

The numbers in many circumstances are unconscionable. California State Teachers Retirement System returned 1.4% in fiscal year end June 30. Their target was actually 7.50%. Springfield, Illinois owes $21 million to pay police and firefighter pensions. That doesn’t sound too bad until you realize the $21 million represents 98% of all property tax revenues. According to Standard & Poor’s, the city of Houston, Texas has racked up pension costs from 2012 to 2015 that rose 48%. What will they do? Issue $1 billion in POBs—a hail Mary pass if ever there was one.

You are probably wondering why pension funds don’t reduce their assumed rates of return to something realistic. Like taking their 7.50% fantasy returns to a more logical 4% to 5% return. The reason is simple. Such target rate of return reductions require real cash infusions to make up the difference.

So we find ourselves at the tail end of an equity bull market that began in March 2009 and a 30-plus year bond bull market. And yet pensions remain woefully underfunded.

The best objective source of research comes from PEW Research. Google PEW Research, unfunded pension liabilities. You’ll find analyses on states and city funding gaps, states in the worst and best shape, data on the 50 state trends, and retiree health care trends. It all adds up to dismal funding for many cities that made promises to pensioners they simply cannot keep.

So why the rant? As the problem gets worse and being we are at the tail end of this credit cycle, general obligation municipal bonds issued by these same states, cities and counties will be severely downgraded. More nails in the coffin that GOs should no longer be the darlings of your municipal bond portfolio .

Connect the dots. As pension funding takes more and more revenue from their general funds, more GO bonds will have to be issued for essential services—schools, roads, welfare, the homeless. All will create a giant revenue sucking sound while essential services deteriorate. The reasons are precisely why revenue bonds—specific revenue bonds—are more desirable than GOs.

Invest in senior airport revenue bonds from major U.S. airports—no local mini airports. Names like Atlanta Hartsfield, Los Angeles International, Dallas Fort Worth, JFK and San Francisco. Major city senior airport revenue bonds are my top pick now.

If you are seeking more yield than airport revenue bonds, then selectively buy hospital revenue bonds. Not your local hospital, but major institutional teaching hospitals like Stanford, Mayo Clinic, Mount Sinai, Cedars-Sinai, University of Colorado Hospital, to name a few.

The weather report declares an unfunded pension tsunami. Please prepare so your portfolio doesn’t drown.

Forbes

by Marilyn Cohen, Contributor

SEP 26, 2016 @ 12:39 PM

Marilyn Cohen is president of Envision Capital Management, Inc., a Los Angeles fixed-income money manager.

Opinions expressed by Forbes Contributors are their own.

New Jersey is on the brink of realizing the American Dream — if the definition is a mega-mall in the middle of a marsh.

A state agency approved $1.2 billion of tax-exempt municipal bonds for Canadian developers Triple Five Worldwide. The company plans to complete a partially built “world-class destination” of shops, restaurants and entertainment attractions in the Meadowlands, 10 miles west of Manhattan, where previous developers ran out of money.

The Sept. 15 decision to float the bonds reignites a debate in New Jersey over the use of government subsidies to foster economic development. Buyers of the bonds won’t pay federal tax on the income, making U.S. taxpayers silent partners in the project. And in addition to paying a lower interest rate than they would on taxable bonds, the developers get a $390 million state grant over time if they reach sales-tax targets.

“It’s essentially crony capitalism,” said Republican State Senator Michael Doherty, who represents a west-central New Jersey district. “Our credit rating is in the crapper and we’re going to triple down by giving more than $1 billion to a private mall developer.” The state has halted non-emergency road improvements for lack of money and faces an $80 billion pension deficit.

Boost Economy

To supporters, American Dream promises to boost New Jersey’s economy, which lagged the U.S. through most of the recovery. The state’s Economic Development Authority estimates it will generate $340 million in state tax revenue over 20 years and create about 11,000 full- and part-time jobs at the complex and 5,800 construction jobs.

“We’ve had false starts,” said James Cassella, mayor of East Rutherford, New Jersey, where the complex sits unfinished. “Hopefully this time is real.”

The 2.9 million square-foot (270,000 square-meter) American Dream, originally called Xanadu, features an indoor amusement park and water park, an 800-foot (245-meter) indoor ski slope, a 300-foot Ferris wheel, aquarium, 1,500-seat performing-arts theater, skating rink and a 1,400-seat movie theater with “wind, rain, snow, fog and scents all synchronized to the on-screen action,” the company says. It will also have 500 stores, restaurants and food shops.

MetLife Stadium

The project broke ground in 2004 across the highway from what is now MetLife Stadium. Construction was abandoned after Mills Corp. and Mack-Cali Realty Corp. and then Colony Capital LLC ran short of funding.

Every day for the last 10-plus years, hundreds of thousands of people pass by what looks to be aging, scattered hunks of metal and concrete, painted in checkerboard shades of pastel blue and orange near the New Jersey Turnpike and within sight of NJTransit commuter trains.

Now construction cranes have appeared again.

Triple Five, run by the billionaire Ghermezian family that also owns Mall of America in Minnesota and West Edmonton Mall in Canada, says it’ll succeed where the others failed. It says the development, slated to open in 2018, will offer plenty to entice an estimated 40 million annual shoppers and thrill-seekers from all over the area and the world.

Tax Dollars

“This will bring much-needed jobs and tax dollars back to our region,” said Rick Sabato, president of the Bergen County Building and Construction Trades Council.

Critics say the development will suck business away from existing enterprises. Paramus, New Jersey, 10 miles north, has three indoor malls, including the 2.1 million square foot Garden State Plaza, owned by Westfield Corp.

The nonprofit New Jersey Alliance for Fiscal Integrity asked a state court last week to stop the project, saying the New Jersey Sports and Exposition Authority, which owns the site, violated state law when it authorized the bonds.

Tax exempt

Tax-exempt bonds are normally used for roads, sewers, schools and bridges.

In order for Edmonton, Alberta-based Triple Five to be eligible, a state or local government must finance the project and the company must pay bondholders what’s called PILOT, or payment in lieu of taxes. Triple Five will pay $800 million of the bond debt in this way.

Triple Five won’t pay property taxes to its host town either. Instead, East Rutherford will receive an upfront payment of more than $20 million from the bond sale and annual payments starting at $750,000 when American Dream opens. Triple Five will also make infrastructure improvements to smooth traffic.

A Brookings Institution report this month found that, since 2000, tax-exempt financing of professional sports stadiums has siphoned $3.7 billion from federal revenue. The report didn’t mention malls.

Rather than sell bonds to the public, the Sports and Exposition Authority will sell them to the Wisconsin Public Finance Authority, which will in turn market its own debt to the public. Tony Armlin, Triple Five’s vice president of development and construction, said the Wisconsin agency charges lower issuance fees.

New Jersey officials have said New Jersey taxpayers won’t be at risk if the bonds default.

Goldman Sachs Group Inc. is managing the tax-exempt bond issue for Triple Five.

Rug Merchant

Don Ghermezian, president of Triple Five, is the grandson of Jacob Ghermezian, an Iranian rug merchant who moved to Canada in 1964. The family built a real estate empire that also includes banking and energy divisions.

Triple Five is investing $300 million in cash and borrowing another $1.5 billion through a construction loan arranged by Deutsche Bank AG.

Triple Five, which says it’s leased 70 percent of the complex, is forecasting $1.5 billion in annual retail sales, even though Bergen County is the last county in the country with a ban on Sunday shopping.

Political Contributions

Bloomberg News reported that members of the Ghermezian family and their employees contributed $40,000 to the New Jersey State Republican Committee in May and $50,000 to the Republican National Committee in June, according to campaign-finance records.

“It’s indicative of a sick economy in New Jersey that you keep having to do these special deals for connected people,” said Doherty, the state senator.

American Dream may end up providing ammunition to critics of the tax-exemption for municipal bonds, said Lisa Washburn, a managing director at Municipal Market Analytics.

New Jersey is “bending over backwards to provide tax-exempt financing along with a whole host of other sweeteners in order to get a non-essential project, benefiting a for-profit company,” Washburn said. “It just doesn’t look good.”

Bloomberg Markets

by Martin Z Braun

September 26, 2016 — 2:00 AM PDT

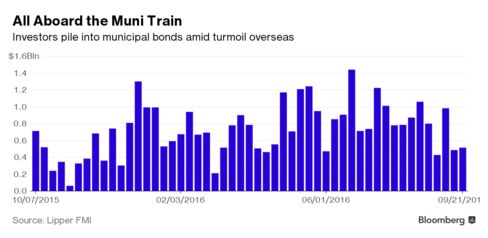

Investors have plowed money into municipal-bond funds for almost a year, allowing local governments to borrow at near record-low yields. That’s making it easier to ignore the cracks beneath the market’s surface.

This week may mark the 52nd straight one with inflows into state and local-government bond funds, the longest streak since 2010, according to Lipper US Fund Flows. Even with the influx, the securities are headed toward the biggest monthly loss since February 2015 on speculation the Federal Reserve may raise interest rates in December. If investors start yanking money out, that could weigh on prices because securities firms have pulled back from the market.

“There’s this anxiety that’s looming under the surface where people are saying, everything is going really well, there’s all these muni inflows but what happens if that stops suddenly?” said Katie Koster, a managing director in public finance investment banking for Piper Jaffray Cos. in Laguna Beach, California. “How will the markets react? They could seize up quite quickly.”

The municipal market has been whipsawed in the past when mom-and-pop investors dumped their bonds en masse. Prices tumbled in late 2010 amid concern the recession would trigger a wave of defaults, a fear that later proved unwarranted. The securities dropped again in 2013 during the so-called taper tantrum, when then-Fed Chair Ben Bernanke jarred investors with plans to scale back the central bank’s bond purchases.

The influx of cash for the past year has been fostered by stock-market volatility and negative interest rates overseas, which have made even rock-bottom municipal yields attractive by comparison. Foreign buyers, who don’t benefit from U.S. tax breaks tied to the debt, increased their holdings to $89.7 billion at the end of June from $74 billion three years earlier.

The streak of cash “shows strong investor demand for an income-producing asset class that has high credit quality, low volatility and continues to act as a diversifier against equity and equity-like risk,” said Sean Carney, head of municipal strategy at BlackRock Inc., which manages about $124 billion of municipal debt. “There’s no indication that flows are about to turn negative, just less robust.”

Municipals have produced a return of 4 percent in 2016, according to Bank of America Merrill Lynch data, thanks to a rally that came as the Fed held off on interest-rate increases that were anticipated this year. The central bank indicated this month that the case for tightening monetary policy has strengthened, and the securities posted a loss of 0.5 percent in September.

Despite the wall of cash that’s allowed even junk-rated borrowers to issue debt, governments continue to deal with mounting pension-fund shortfalls that are exerting a drag on their credit ratings. And the impact of a selloff could be exaggerated by the brokerage industry’s diminished role in the market since new regulations went into effect after the financial crisis: Dealers’ holdings fell to about $20 billion at the end of June, down by half from $40 billion in mid-2011, according to Fed data.

“Investors have to be careful about not lulling themselves into a false sense that this abundant liquidity in the market right now is driven by dealers,” said James Iselin, head of the municipal fixed income team in New York at Neuberger Berman, which oversees about $10 billion. “It’s really driven by investors and asset managers who have pumped a lot of money into the space.”

To prepare, he said investors should buy bonds from highly-rated governments even if they offer less yield than more speculative ones.

“Giving up a little bit more to be more flexible and nimble for an environment that could be less liquid, that’s a trade that investors should certainly think about right now,” he said.

But with the interest rates so low, investors have been doing the opposite, said Piper Jaffray’s Koster. “That could be a problem down the road.”

Bloomberg Markets

by Romy Varghese

September 28, 2016 — 2:00 AM PDT

Taylor Riggs, a contributor to Bloomberg Briefs, talks with Joe Mysak about this week’s municipal market news.

A group of U.S. senators introduced a bipartisan bill that includes municipal bonds among assets that banks need to hold to weather a financial shock.

Democratic Senators Mark Warner and Chuck Schumer and Republican Mike Rounds introduced a scaled-down version of legislation that passed the House in February that would classify investment grade municipal bonds on par with U.S. agency securities issued by Fannie Mae and Freddie Mac to meet bank liquidity rules.

The Senate measure classifies munis as “Level 2B” assets comparable to certain corporate bonds and stocks.

Level 2B assets are subject to a 50 percent “haircut,” meaning if a bank holds $1 million of a municipal bond, $500,000 counts towards its liquidity buffer. The House bill classifies munis as Level 2A assets, which have a 15 percent haircut. Level 2A and 2B assets can make up no more than 40 percent of total “high quality liquid assets,” with Level 2B assets restricted to no more than 15 percent of HQLA.

“As a former governor, I know firsthand how critical it is for states and municipalities to issue bonds that fund their basic operations, including the construction of schools, roads, and local projects,” Warner said in a news release “We must ensure a continued and reliable access to capital markets for our local governments, and this legislation represents a compromise that achieves that while appropriately balancing concerns for the long term stability of our financial system.”

Local-government officials and securities-industry lobbyists turned to Congress after regulators including the Fed adopted rules that would restrict or bar banks from including munis among high quality liquid assets. State treasurers and city finance officers said the new rules, if not changed, will saddle them with higher borrowing costs eliminating incentives banks have to purchase the bonds.

“Having bipartisan, bicameral legislation is an excellent first step,” said Emily Brock, federal liaison for the Government Finance Officers Association. “It shows a commitment on their part for what we municipal securities to be, which is high quality and liquid.”

Bloomberg Markets

bu Martin Z Braun

September 27, 2016 — 10:07 AM PDT Updated on September 27, 2016 — 1:36 PM PDT

The privately run prison in Walnut Grove, Mississippi, was besieged for years by violence and legal fights over deplorable conditions. Then last month, with local sentencing reforms keeping fewer behind bars, officials shut it down, leaving the state on the hook for $121 million of debt left behind.

“The taxpayers are paying for that building and it’s just sitting there,” said Chip Jones, an alderman for the 1,600-person town about 63 miles (101 kilometers) east of Jackson, the state capital.

The closing is part of a shift taking place nationwide among states and local governments that have sold $30 billion of bonds to build prisons and jails, some of which were leased to for-profit operators. With officials re-evaluating tough-on-crime laws that caused inmate populations to soar and the federal government moving to jettison its use of private prisons, the reduced need for such facilities is rippling through a niche of the $3.8 trillion municipal-securities market.

On Friday, a Texas prison that serves as a U.S. detention center had its credit rating cut to junk by S&P Global Ratings, joining half a dozen others that were downgraded below investment grade by the company since federal officials in August announced plans to phase out for-profit facilities. About $300 million of tax-exempt debt issued for almost two dozen prisons has already defaulted, and investors are demanding higher yields on other securities amid speculation the distress will spread.

“At any point there are only so many prisoners out there to fill the private prison beds,” said Matt Fabian, managing director for Municipal Market Analytics Inc. “It creates unequal distribution and you have prisons competing against one another.”

The number of Americans behind bars has been on a steady decline. After peaking at 1.62 million in 2009, the state and federal prison population dropped over the next five years, reducing it by 54,000, or 3 percent, by 2014, the most recent year for which figures are available, according to the U.S. Bureau of Justice Statistics.

It’s not certain that such reductions will continue, said Daniel Hanson, an analyst who follows the municipal-bond market for Height Securities in Washington. Even with the decrease, some federal prisons are still over capacity and states may already have done much of what they can to keep non-violent offenders out of their penal systems, he said.

“The low hanging fruit of criminal-justice reform is already done,” said Hanson.

At the federal level, the impact is poised to trickle down. The Department of Justice on Aug. 18 said it will cancel or scale back the scope of private prison contracts after the number of federal inmates fell by about 25,000 over the past three years. About two weeks later, the U.S. Department of Homeland Security, which houses immigration detainees in privately run facilities, said it will review whether to curb their use too.

Such a step would jeopardize the repayment of local-government bonds issued for prisons, which are typically repaid with revenue from leasing them instead of with taxpayer money. Since August, S&P has lowered to junk debt issued by, among others, the Washington Economic Development Financing Authority, the Garza County Public Facility Corp. in Texas, and the La Paz County Industrial Development Authority in Arizona.

The prices of some securities have tumbled, pushing up the yields as investors demand higher compensation for the risk. The yield on bonds issued for the Reeves County detention center in Pecos, Texas, which mature in 2021 and were among those downgraded, rose to as much as 6.4 percent last month from 4.6 percent in early August.

Additional closures could spread the impact. In Florence, Arizona, a 31,000-resident town southeast of Phoenix, the seven prisons — four of which are privately-run — are a major employer, said Jess Knudson, town spokesman. One of them is an immigration facility that could be hit if Homeland Security follows Justice’s lead.

“Our ability to influence that decision doesn’t exist,” Knudson said.

The Mississippi Department of Corrections closed the Walnut Grove prison because of budget constraints and the number of inmates, with the annual average population dropping by about 10.5 percent between fiscal 2011 and 2016, bond documents show.

The decline was driven in part by the passage of criminal-justice reform that gave judges more discretion over sentencing, according to the Pew Charitable Trusts, which partnered with a state task force to push the 2014 law. The measure is projected to save the state $266 million over 10 years while also “safely reducing” the number of inmates, the group said.

With less need for prison beds, Mississippi chose to shut down a facility that had a troubled history under former operator Geo Group. After it was sued by inmates, the Justice Department faulted it in 2012 for widespread staff misconduct and deliberate indifference to the welfare of the young offenders housed there.

A federal judge said the description of life inside painted “a picture of such horror as should be unrealized anywhere in the civilized world.”

Mississippi said it has been pleased with Management and Training Corp., the for profit company that took over Geo Group after the Justice Department investigation.

The prison was closed last month and its 900 inmates were moved to other facilities. Mississippi still owes $121 million of debt for Walnut Grove, which the department of corrections has an “absolute and unconditional” obligation to pay off, according to bond documents. There state is considering using the emptied prison for another purpose.

“Anything’s better than nothing,” said Jones, the local alderman. “The taxpayers are paying for that building, and it’s just sitting there.”

Bloomberg Markets

Amanda Albright and Darrell Preston

October 3, 2016 — 2:00 AM PDT Updated on October 3, 2016 — 7:45 AM PDT

Fitch Ratings-New York-03 October 2016: Growth for the remainder of 2016 will remain healthy for all three U.S. major transportation sectors (airports, ports and toll roads) albeit at a slightly lower rate than the first half of the year, according to Fitch Ratings in a new report.

Fitch expects passenger traffic growth to increase around 3% for the second half of 2016 (2H16), with the bulk of air passenger growth coming from international hub airports. All but one major U.S. carrier has seen positive traffic growth through the first part of 2016, though a wide range of performance continued. JetBlue (12.1%) and Southwest Airlines (7.8%) led the way with strong increases in revenue passenger miles while increases among American Airlines (1.9%) and United Airlines (-0.1%) were more marginal.

Ports nationwide will continue to benefit from a stronger dollar driving imports, with 20-foot equivalent units (TEUs) growing at a level above GDP for the 1H16. A primary focus for ports remains “big ship readiness”. That said, shippers, logistics providers and ports will be keeping close watch over the expanded Panama Canal, which opened for commercial traffic this year. While large-scale shifts in cargo are not expected, some adjustments are possible.

As for toll roads, low fuel prices have boosted growth in traffic (6.3%) and revenue (7.0%) for the 1H16. The Southeast and Southwest U.S. have and will continue to lead in traffic performance. The higher rate of growth in revenues is reflective of typical inflationary toll rate increases, which Fitch expects to average roughly 2% over time.

A degree of uncertainty always remains for the long-term direction of the broader economy.

The Transportation Trends report includes an expanded data set in its appendices, including six-month year-to-date 2016 volume and revenues, six-month percentage change year-over-year for volume and revenue, 2015 full year volume and revenues, 2010-2015 five-year compounded annual growth rates, and recessionary peak-to-trough data. ‘U.S. Transportation Trends’ is available at ‘www.fitchratings.com’ or by clicking on the above link.

Contact:

Seth Lehman (Airports)

Senior Director

+1-212-908-0755

Fitch Ratings, Inc.

33 Whitehall Street

New York, NY 10004

Emma Griffith (Ports)

Director

+1-212-908-9124

Tanya Langman (Toll Roads)

Director

+1-212-908-0716

Media Relations: Sandro Scenga, New York, Tel: +1 212-908-0278, Email: [email protected].

Additional information is available at www.fitchratings.com.

Fitch Ratings-New York-22 September 2016: Despite balance sheet contractions, State Housing Finance Agencies (SHFA) have increased overall equity, according to a Fitch Ratings report.

In FY 2015, aggregate adjusted equity rose 2.6% from FY 2014 levels and increased 15.9% from FY 2010 levels.

Marking the fifth straight year of across-the-board declines, aggregate SHFA assets decreased by 0.8%; aggregate debt fell by 2.9%; and aggregate loans declined by 1.8%. Albeit at a reduced rate of decline compared with recent fiscal years, these decreases are reflective of the economic and mortgage-lending environments during that period and the shift in SHFAs’ business model in response.

“FY 2015 contained the same challenges for SHFAs as the past several years. Low interest rates continued to suppress investment income and low conventional mortgage rates decreased the volume of SHFA-issued debt for originating new whole loan mortgages,” said Ryan Pami, Associate Director.

“SHFAs sought other ways to remain profitable, such as originating loans through the to-be-announced market, utilizing direct sales of MBS and issuing MBS pass-through instruments. Despite the challenging environment, FY 2015 results demonstrated that SHFAs are financially sound, as median ratios, such as Net Interest Spread, Net Operating Revenue and Debt-to-Equity (DTE), continued to trend positively.”

Leverage ratios continued to improve as the median adjusted DTE ratio declined to 3.1x in FY 2015 from 3.4x in FY 2014. This is significantly lower than the five-year average median and the FY 2010 median, which were 3.9x and 5.5x, respectively, and now stands as the lowest median DTE ratio in the past decade.

For more information, a special report titled “State Housing Finance Agencies – Peer Study” is available on the Fitch Ratings web site at www.fitchratings.com.

Contact:

Ryan J. Pami

Associate Director

Fitch Ratings, Inc.

+1-212-908-0803

33 Whitehall Street

New York, NY 10004

Ronald McGovern

Senior Director

+1-212-908-0513

Media Relations: Elizabeth Fogerty, New York, Tel: +1 (212) 908 0526, Email: [email protected].

Additional information is available at ‘www.fitchratings.com’.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTP://FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY’S PUBLIC WEBSITE ‘WWW.FITCHRATINGS.COM’. PUBLISHED RATINGS, CRITERIA AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH’S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE ‘CODE OF CONDUCT’ SECTION OF THIS SITE. FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO THE RATED ENTITY OR ITS RELATED THIRD PARTIES. DETAILS OF THIS SERVICE FOR RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE.

WASHINGTON — A bipartisan group of senators is pushing to include municipal bonds in bank-safety rules, the latest wrinkle in a continuing fight over how safe—and salable—the debt of states and localities would be in another financial crisis.

Sens. Mark Warner (D., Va.), Charles Schumer (D., N.Y.) and Mike Rounds (R., S.D.) are set to introduce legislation on municipal bonds this week, according to Senate aides. The bill aims to open the door for big U.S. banks to count municipal bonds as liquid assets under rules completed in 2014 that were designed to ensure Wall Street firms have enough cash during a crisis to fund their operations for 30 days.

The Senate legislation would place municipal bonds on the lowest rung of the “high quality liquid assets” category. That means they would be treated on par with corporate bonds, but not as favorably as under related legislation approved by the House early this year.

“We must ensure a continued and reliable access to capital markets for our local governments,” Mr. Warner said in a written statement. “This legislation represents a compromise that achieves that while appropriately balancing concerns for the long term stability of our financial system.”

The rules, slated to go into effect next year, are aimed at making banks hold more cash or securities that are easy to sell. The Federal Reserve and two other bank regulators had originally decided debt issued by states and localities didn’t make the cut—prompting a backlash from banks, lawmakers and states and localities who warned the move would make the bonds less attractive and raise borrowing costs for municipalities.

The Fed completed amendments in April to allow some investment-grade municipal bonds to qualify. But the two other regulators involved in the rules—the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp.—haven’t followed suit.

Aides to Senate lawmakers say their bill was scaled back from the House version to gain broad support for it in the Senate, though it is unclear if there is sufficient time in the remaining year to advance the bill.

Sen. Richard Shelby (R., Ala.), chairman of the Senate Banking Committee, indicated earlier this year that he was reluctant to second-guess banking regulators that originally excluded municipal bonds when they wrote the rules in 2014. But an aide to Mr. Shelby said he wouldn’t object to the coming bill as it incorporates changes the Fed already adopted in its version of the rules.

Banks underwrite muni bonds, buy them as investments and sell them to clients. Lenders have played an increasingly central role in the thinly traded, $3.7 trillion market and are now the biggest buyers of municipal debt, according to Municipal Market Analytics Inc., a research firm.

Municipal officials have generally applauded the Fed’s willingness to make changes to the rules but say legislation is necessary, largely because banking firms typically hold municipal debt in units that are overseen by the other policy makers involved in the rules, particularly the OCC, which regulates national banks.

Officials at the OCC remain dismissive of including the municipal bonds in the rules and don’t believe the debt is sufficiently liquid, according to people familiar with their thinking. The FDIC is waiting until the rules go into effect next year before considering amending its version, according to people familiar with that agency.

While the Senate bill would rank municipal debt similarly to the Fed’s amended rules—allowing the banks to count 50% of the bonds’ face value when including them in their funding buffers—the legislation would allow banks to include more types of municipal bonds, a Senate aide said.

These include revenue bonds, or securities backed by a specific revenue stream, that comprise the bulk of debt issued by states and local governments but that are kept out of the current Fed version of the rules.

The House bill, meanwhile, is broader than both the Senate bill and the Fed’s version of the rules, allowing banks to count 85% of the bonds’ face value.

To date, banks have by and large continued to hold lots of municipal bonds despite the rules, in part because they are seen as less risky than corporate debt and are priced competitively to other types of debt, according to bank officials. If interest rates rise this year, banks are expected to begin to pare their muni holdings.

Corrections & Amplifications:

An aide to Sen. Richard Shelby (R., Ala.), chairman of the Senate Banking Committee, said he wouldn’t object to the coming municipal bond legislation. An earlier version of this story said an aide to Mr. Shelby said he would support the bill. Also, these comments were made by an aide to Sen. Shelby. Due to an editing mistake, an earlier correction to this story erroneously cited Sen. Shelby for these remarks.

THE WALL STREER JOURNAL

By ANDREW ACKERMAN

Updated Sept. 27, 2016 10:27 a.m. ET

Write to Andrew Ackerman at [email protected]

J.P. Morgan, Nuveen invest in school board’s bonds at big profit

The Chicago school system needed money—fast. Two Wall Street players saw an opportunity to invest.

J.P. Morgan Chase & Co. and Chicago-based Nuveen Asset Management have made realized and paper profits exceeding $110 million on purchases this year of $763 million in Chicago Public Schools bonds. The school system has said it needed the money to replenish its dwindling coffers before the new school year and to build and repair facilities.

The terms of the bond sales highlight the choices the school district faces after years of pension shortfalls and relying heavily on borrowing. The 397,000-student school district struggled to sell municipal bonds in February until Nuveen bought about one-third, and the district decided in July to borrow directly from J.P. Morgan for fear that investors might balk again, a spokeswoman for the Chicago Board of Education said.

“CPS did not have the luxury of waiting longer to demonstrate to the market that the progress we were making was real,” said Ronald DeNard, the school district’s senior vice president of finance, in an emailed statement about the bonds purchased in July by J.P. Morgan.

J.P. Morgan, the country’s largest bank by assets, made a 9.5% profit on $150 million in bonds it bought in July and sold in September, or 82% annualized. Nuveen, an investment firm managing $160 billion, has bought $613 million in bonds since February for a total return, including price gains and interest payments, of about 25%. That is almost 50% on an annualized basis, an especially large gain at a time of near-zero interest rates.

The school system’s bonds are a favorite for John Miller, Nuveen’s co-head of fixed income, who said the firm bought when the market feared a default, a concern he called overblown. “At the end of day, this school system is critically important to Chicago—to the whole country really,” he said.

Its bonds are rated B3 by Moody’s Investors Service and traded as low as 73 cents on the dollar in March before rebounding to about 90 cents in September. CPS said the bond sales facilitated much-needed fixes like lead abatement and classroom construction, though they increased the school system’s already heavy debt load and its annual interest payments.

“We took a period of market risk on behalf of our client when they needed it most and the market has recognized their improved financial position,” a J.P. Morgan spokeswoman said.

Chicago’s school district operates on a budget of $5.5 billion with a below-investment-grade, or junk, credit rating on nearly $7 billion of bonds. Its teachers union is threatening to strike, in part, over proposed changes to its pension plan, which has a nearly $10 billion funding gap. The school system’s rainy-day fund is nearly empty and relies on short-term borrowing.

“J.P. Morgan and Nuveen are taking advantage of a distressed school district at the expense of our most vulnerable students,” said Jackson Potter, staff coordinator at Chicago Teachers Union.

Nuveen held few Chicago Public School bonds in recent years but has been watching its prices closely since May 2015, when Moody’s cut its credit ratings of the school board and the city of Chicago to junk.

The investment company, which now owns about $806 million of the school district’s bonds, dedicated an analyst to cover the district full time to better understand its capacity to increase revenue and the likelihood of a bankruptcy filing.

Prices of outstanding Chicago school bonds were hit in 2013 and 2015 after defaults by Detroit and Puerto Rico. Illinois Gov. Bruce Rauner called for a state takeover of the school system and for a potential bankruptcy filing over the past year and prices fell below 75 cents on the dollar.

Nuveen determined that the default risk was far lower than that implied by the bond prices. When J.P. Morgan was struggling to find buyers of $725 million in bonds in February, the fund manager agreed to buy about 36% of the issue at about 84 cents on the dollar.

Mr. Miller continued buying after and now owns 60% of the bonds, making it the single largest investment in the $15 billion Nuveen High Yield Municipal Bond Fund. Nuveen has made unrealized gains of about $103.3 million on all the CPS bonds it owns, a company spokeswoman said.

Demand for Chicago Board of Education debt grew over the summer as investors gained confidence that the school board could plug much of its 2017 budget gap with budget cuts, state aid and new tax revenues. Market conditions also improved significantly, sending prices of municipal bonds with junk credit ratings up and pushing their yields down to about 4.6% in early July, a 17-year low, according to the S&P Municipal Bond High Yield Index.

Still, when the school district turned to J.P. Morgan for more money in July, it decided to sell the bonds directly to the bank to avoid the risk that investors would reject it. Instead, demand for the bonds rose throughout the summer, and J.P. Morgan sold all of the debt for a $12 million profit in September, Wall Street Journal analysis of data from the Municipal Securities Rulemaking Board shows.

“You’ve gone from having maybe two to three people being interested in these deals to all of a sudden having 20 investors interested,” said Mr. Miller of Nuveen.

J.P. Morgan committed to hold the $150 million in bonds it purchased for about six weeks until the board of education prepared documentation allowing them to be sold to institutional investors.

The certainty J.P. Morgan provided came with a high price: The bank paid 91 cents on the dollar for the debt at a yield of 7.25%, much higher than the approximately 6% yield on the school board’s outstanding bonds at the time. It sold the debt at prices as high as 102 cents on the dollar in early September and its trading profits, plus a $1.2 million purchaser’s fee, amount to the 9.5% return in six weeks.

J.P. Morgan has a longstanding relationship with Chicago Public Schools and is the top underwriter of its bonds over the past 10 years, according to data from Thomson Reuters. The bank views the school board as a high-priority client that it understands well and is willing to support its short- and long-term capital needs, the bank spokeswoman said.

THE WALL STREET JOURNAL

By MATT WIRZ and HEATHER GILLERS

Updated Oct. 2, 2016 11:31 p.m. ET

—Aaron Kuriloff

contributed to this article.

Write to Matt Wirz at [email protected] and Heather Gillers at [email protected]

CHICAGO — Bonds sold by U.S. states, cities, schools and other issuers in the municipal market could be held as liquid assets by banks under legislation introduced on Tuesday in the U.S. Senate, bolstering the case for purchasing the debt while helping financial institutions weather market crises.

The bipartisan measure would classify high-quality municipal bonds at the same level as corporate debt, allowing banks to use munis to comply with new 30-day federal liquidity requirements.

Federal rules approved in 2014 and effective next year are aimed at ensuring big banks will be able to access sufficient cash during a financial crisis. But the rules excluded muni bonds from the types of securities that count as high quality liquid assets, or HQLAs.

Muni debt issuers fear the exclusion would deter banks from buying muni debt, hurting their ability to fund everything from schools and bridges to water treatment plants and hospitals.

“If banks retreat from the muni-bond market, it could choke off a critical source of investment on which our cities and localities rely. This bill protects the stability of our markets while providing continued access to muni bonds for local governments,” Senator Chuck Schumer, a New York Democrat, said in a statement.

Schumer, along with Senators Mark Warner, a Virginia Democrat, and Mike Rounds, a South Dakota Republican, led a group sponsoring the legislation.